AML supervision in the Czech Republic and across the EU is clearly tightening. Data from the Financial Analytical Office (FAÚ) and European regulatory developments point to the same trend: more inspections, more administrative proceedings, and significantly higher fines. This is not a fluctuation — it is a structural shift that will continue.

Table of contents

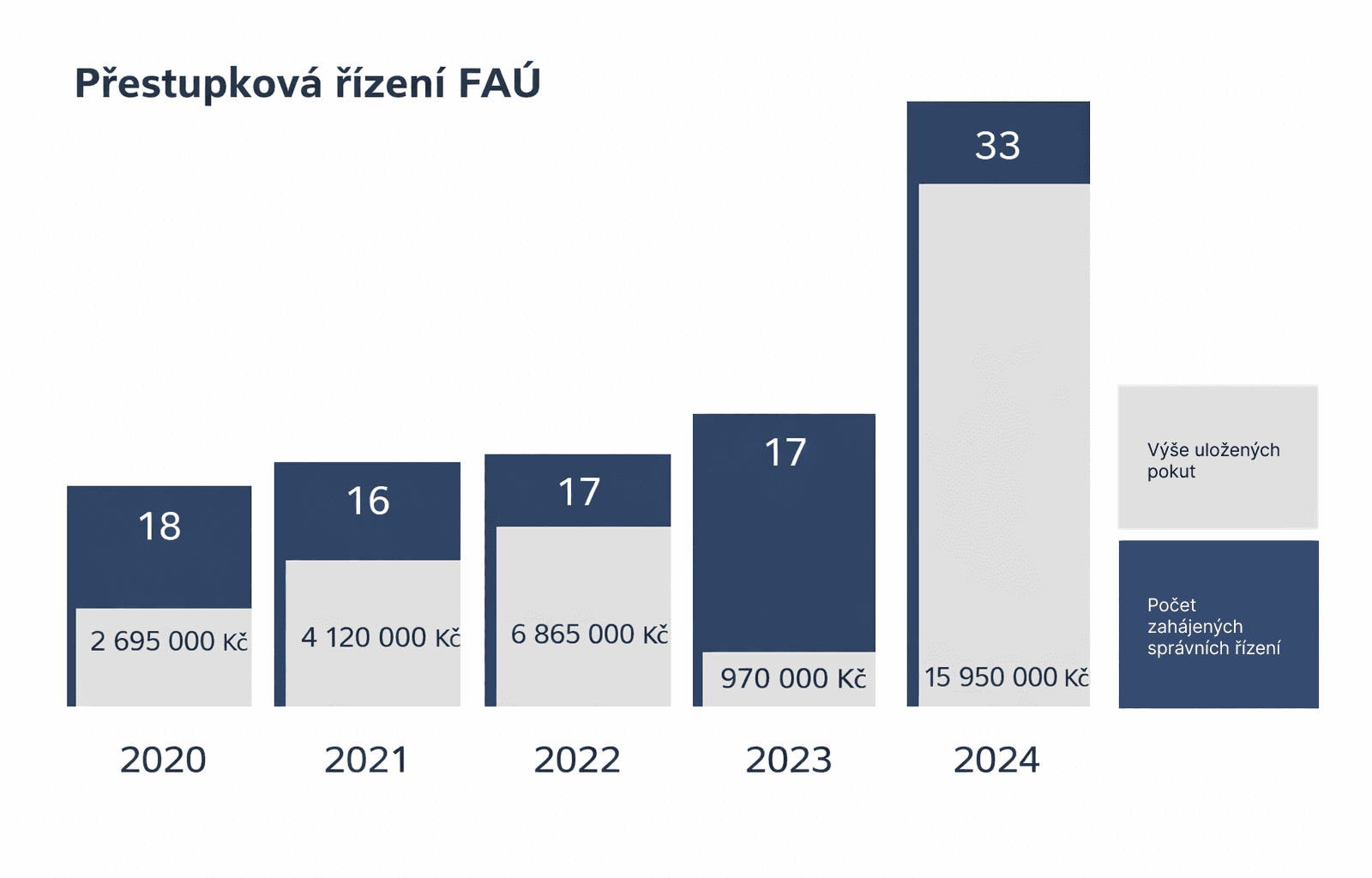

Hard Data from the Czech Republic: FAÚ Is Picking Up the Pace

FAÚ statistics from recent years show a clear trajectory:

- The number of administrative proceedings initiated is steadily increasing

- The total amount of fines varies by case, but in 2024 it reached nearly CZK 16 million (approx. EUR 640K) — a significant jump compared to previous years

- 2024 also set a record for the number of proceedings (33)

While in 2020 the annual fines were in the single-digit millions of CZK, today we are talking about significantly higher amounts and more systematic oversight.

This is not just about banks or large institutions. FAÚ has long been focused on real estate agencies, accountants, lawyers, dealers in high-value goods, and service providers.

A Real-World Case: Real Estate Agency

In 2025, FAÚ imposed a fine on the company:

Molík reality s.r.o.

Reasons for the sanction:

- Failure to meet the reporting obligation under § 46(2) of the AML Act

- Violation of obligations in client identification and due diligence under § 44(1)(a) of the AML Act

A typical scenario from practice: the obliged entity underestimated formal steps often perceived as mere 'paperwork'. From FAÚ's perspective, however, these are the fundamental building blocks of an AML system.

Europe: The Pressure Is Just Getting Started

Czech data must be read in a broader context:

- 2025 brought a rise in AML fines across Europe and the closing of long-running cases

- From 2026, AMLA — the European anti-money laundering authority — will become operational

- AMLR (EU 2024/1624) takes effect — a directly applicable regulation, less room for excuses, more unified oversight

Globally, AML fines surged by 417% between 2024 and 2025. Key trends include massive sanctions from US and European regulators, a strong focus on KYC violations, and growing pressure to leverage artificial intelligence for compliance.

This means:

- Less tolerance for 'paper compliance'

- Greater emphasis on demonstrability, audit trails, and consistent decision-making

- Higher reputational and financial risk for obliged entities

Are you subject to AML?

Enter your company ID (IČO) and instantly find out whether you're subject to AML regulations

What Actually Gets Penalised

From the practice of FAÚ and European regulators, the following violations are most common:

- Missing or purely formal client identification and due diligence

- Failure to report suspicious transactions

- Inconsistent risk assessments

- Non-existent or outdated internal AML policies (SVZ)

- Lack of traceable documentation during inspections

This is not about intentional money laundering. In most cases, it is about process failures.

Conclusion: The Trend Is Clear

AML enforcement has shifted from a 'formal obligation' to a phase of active enforcement. The number of proceedings is growing, fines are increasing, and regulatory pressure will continue to intensify.

For obliged entities, this means one thing: having AML processes truly under control, not just on paper.

That is exactly what AML PROOF is built for — so that compliance is not a scare at inspection time, but a repeatable, audit-safe process.